Fixed Index Annuties

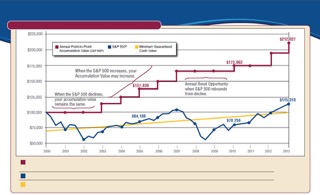

The Annual Reset feature can be powerful in helping you grow and maintain your retirement nest egg. This chart provides an example of the interest credited to an Annual Point-to-Point Fixed Index Annuity Contract in force from October 1, 2000 to October 1, 2013 and shows the value of the Annual Reset feature. The Annual Reset allows for any interest credited on each contract anniversary, to be “locked-in” and it can never be taken away even in years when the index value goes down. The interest credited is added to the premium which then becomes the guaranteed Accumulation Value “floor” that will be included in the calculation of the interest that is credited going forward. The annual reset sets the index starting point each year at the contract owner’s anniversary. This reset feature is beneficial when the index experiences a severe downturn during any given year because not only do you not lose accumulation value from the downturn, but the new starting point for future growth calculations is the lower index value.

As you can see in the chart, the Annual Point-to-Point accomplished growth due to the annual reset design. It offers growth opportunities in years when the S&P 500® has positive returns and protects against loss of premium or previously credited interest in years of negative returns.

The Annual Point-to-Point applies an Index Cap Rate, or upper limit, to calculate the index credits each year. The Index Cap Rate will always be declared on the contract anniversary and guaranteed for that year.

This rate may be changed annually at the Company’s discretion. However, at no time will this rate ever fall below the minimum guarantees. The Minimum Guarantees vary depending on the company and product feature.

The Annual Point-to-Point is not an investment. Rather fixed index annuities can provide powerful benefits, such as:

- Protection Against Market Losses

- Guarantee of Premium

- Annual Reset

- Minimum Guaranteed Cash Value (if applicable)

- Tax-Deferred Growth

- Guaranteed Lifetime Income

- The Potential to Avoid Probate in some states.

As mentioned before, while the accumulation value in this example appears favorable when viewed with performance of the S&P 500® Index, these results are not an indication that Fixed Index Annuities will outperform the S&P 500®.

The history of the above Indexed Annuity demonstrates the powerful benefits of Indexed Annuities with the annual reset interest crediting design. There are current products with reset design as well. This account did exactly what it was supposed to do … give the Contract Owner the opportunity to accumulate value based on the appreciation of the S&P 500® Index, without the risk of loss of Principal in years when the S&P 500® was negative. All of this supported by a minimum guarantee.

This is not an illustration. This is a depiction of an actual policyholder.

These results should not be an indication that Indexed Annuities will outperform the S&P 500®. This simply demonstrates the powerful benefits of Indexed Annuities with the annual reset interest crediting design.

Basic benefits of Indexed Annuities:

- 1. Preservation of Principal

- 2. Reasonable Rates of Return

- 3. Tax-Deferral

- 4. Minimum Guarantees

- 5. Guaranteed Lifetime Income

- 6. Possible Probate Avoidance

* The graph shown was based on actual credited rates for the period shown on the index annuity product at the time which the product was available.

Past performance is not an indication of future results.

**Check our disclosure for additional information. ** The “S&P®” is a product of S&P Dow Jones Indices LLC and has been licensed for use by multiple insurance carriers. “Standard & Poor’s®” and S&P® are registered trademarks of Standard & Poor’s Financial Services LLC (“S&P”); Dow Jones® is a registered trademark of Dow Jones Trademark Holdings LLC (“Dow Jones”); Standard & Poor’s®, are trademarks of the SPDJI; and these trademarks have been licensed for use by SPDJI and sublicensed for certain purposes to insurance carriers. Fixed Index Annuities are not sponsored, endorsed, sold or promoted by SPDJI, Dow Jones, S&P, their respective affiliates and none of such parties make any representation regarding the advisability of investing in such product(s) nor do they have any liability for any errors, omissions or interruptions of the S&P.

United Solutions Advisors do not give legal or tax advice. Consult your own personal advisor regarding these matters.